Table of Contents >> Show >> Hide

- Why Inflation Feels Like the Villain in Everyone’s Story

- What Economists Mean by “Animal Spirits”

- Why Everyone Hates Inflation (Even in a Strong Economy)

- Winners, Losers, and the Uncomfortable Truth About Inflation

- Common-Sense Ways to Protect Yourself from Inflation

- Real-World Experiences: Animal Spirits in an Inflationary World

- Conclusion: Keep Your Cool While Prices Run Hot

If there’s one thing that can unite people across income levels, political views, and favorite streaming platforms, it’s this: everyone hates inflation.

Even when the job market looks strong and economic data doesn’t scream “recession,” people still feel grumpy when prices jump. That emotional reaction is exactly what economists mean by “animal spirits”the mix of confidence, fear, frustration, and vibes that drive how we spend, save, invest, and vote.

In the spirit of A Wealth of Common Sense, let’s unpack why inflation bothers people so much, how animal spirits turn price changes into full-blown narratives about decline and unfairness, and what common-sense moves can actually help you survive (and maybe even benefit from) an inflationary world.

Why Inflation Feels Like the Villain in Everyone’s Story

Inflation isn’t just a number on a government chart. It shows up in your cart, your rent payment, your kid’s tuition, and your utility bill. That’s why you don’t need a PhD in economics to know when prices are risingyou feel it before you read about it.

Most people experience inflation as a simple story:

- “My paycheck doesn’t go as far as it used to.”

- “Stuff I buy all the time is more expensive.”

- “Someone, somewhere, is taking advantage of me.”

Economists might argue about base effects, core versus headline inflation, or whether price spikes are “transitory.” Regular people don’t care about that. They care that their grocery bill went from $120 to $160 while their paycheck barely moved.

That gap between academic theory and real-world experience is the perfect playground for animal spirits: emotions fill in the blanks where facts feel distant or abstract.

What Economists Mean by “Animal Spirits”

From Keynes to Modern Markets

The term “animal spirits” comes from John Maynard Keynes, who argued that the economy is not driven only by cold, rational math. It’s also powered by gut feelingsoptimism, fear, excitement, and panicthat push people to act when the future is uncertain.

In economics and finance, animal spirits show up when:

- Investors pile into hot stocks because “everyone else is making money.”

- Homebuyers stretch budgets because they’re afraid they’ll be “priced out forever.”

- Consumers suddenly pull back on spending because they feel like a downturn is coming, even before the data proves it.

Modern behavioral finance and central bank research support this idea: expectations, narratives, and trust matter as much as spreadsheets. People don’t wait for perfectly calculated forecaststhey react to stories, headlines, and personal experiences.

Inflation as Rocket Fuel for Animal Spirits

Inflation is especially powerful at stirring up animal spirits because it hits so many emotional triggers at once:

- Loss aversion: Paying more for the same thing feels like losing money, even if your income has risen.

- Uncertainty: If prices are jumping now, will they ever stop? Should you rush to buy before they rise again?

- Fairness: If companies are reporting record profits while your bills climb, it feels like the game is rigged.

When those feelings spread across millions of households and businesses, they shape actual economic outcomes: slower spending, more cautious hiring, higher wage demands, and increased pressure on policymakers.

Why Everyone Hates Inflation (Even in a Strong Economy)

1. Inflation Quietly Steals Purchasing Power

The biggest reason people hate inflation is simple: it erodes purchasing power. When prices rise faster than wages, your lifestyle slowly shrinks, even if your nominal paycheck looks bigger on paper.

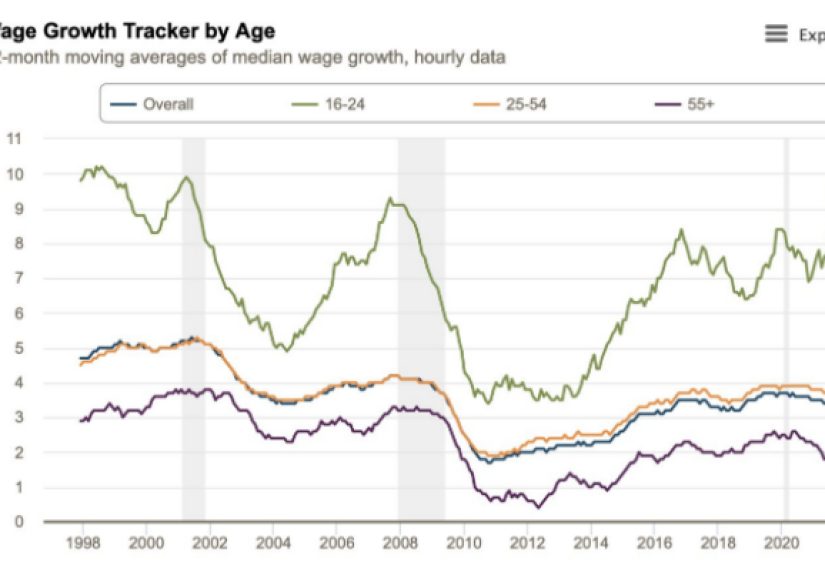

Over the past few years, many U.S. households have watched prices climb faster than their income. Even small gaps between wage growth and inflation add up over several years, making everyday life feel tighter. That squeeze is especially painful for lower- and middle-income families who spend most of their income on essentials like food, housing, transportation, and utilities.

2. It Makes Planning Feel Impossible

Inflation isn’t just about today’s prices. It messes with your ability to plan for tomorrow.

- How do you build a multi-year budget when rent increases are unpredictable?

- How do you design a retirement plan if you’re not sure what your cost of living will be in ten years?

- How does a business commit to a big investment when it can’t confidently forecast costs or consumer demand?

This uncertainty pushes people toward either paralysis (“I’ll just wait and see”) or rushed decisions (“I better buy now before it gets worse”). Neither extreme is ideal for long-term financial health.

3. It Feels Deeply Unfair

One of the most interesting findings from surveys and economic research is that people don’t just see inflation as a math problemthey see it as a fairness problem.

When prices rise, many people assume:

- Companies are “price gouging” or taking advantage of crises.

- The system is rewarding asset owners and punishing workers.

- Politicians are out of touch because they don’t feel the same pressure at the checkout line.

At the same time, people rarely attribute their own pay raises to inflation. They tend to interpret higher wages as personal achievement, not as compensation for higher prices. So when they see prices rising again, they feel like they’re being asked to pay twice.

4. The Emotional Impact Lingers Longer than the Data

Even when inflation rates start to fall, the emotional damage doesn’t disappear overnight. People remember the painful years. If your grocery bill jumped 20% over a few years, you don’t feel much better just because the rate of increase slows down from 8% a year to 3%.

In other words, inflation can come down, but the level of prices stays elevated. That’s why surveys often show that consumer sentiment remains gloomy long after official inflation metrics look “under control.” Animal spirits run on memory, not just on monthly reports.

Winners, Losers, and the Uncomfortable Truth About Inflation

Here’s where common sense and nuance collide. While most people dislike inflation, not everyone is hurt equallyand some are quietly helped by it.

Who Loses the Most?

- Wage earners whose pay doesn’t keep up: If your salary lags inflation for several years, your real income falls and it becomes harder to save or invest.

- Retirees on fixed incomes: Without cost-of-living adjustments, rising prices can rapidly erode the value of pensions or savings.

- Cash-heavy households: If your money sits mostly in checking or low-interest savings accounts, inflation quietly eats away at its value.

Who Might Benefit?

- Borrowers with fixed-rate debt: If you locked in a low mortgage rate before inflation spiked, you repay that debt with “cheaper” future dollars.

- Owners of real assets: Housing, certain types of businesses, and some commodities can rise in value with inflation, preserving or increasing purchasing power.

- Investors in productive companies: Firms with pricing power and strong balance sheets may pass along higher costs and maintain profits, benefiting shareholders.

That doesn’t mean inflation is “good” for these groupsit just means the picture is more complicated than “inflation hurts everyone equally.” But because most people experience inflation through everyday spending rather than balance sheet effects, the dominant emotion remains: we hate this.

Common-Sense Ways to Protect Yourself from Inflation

1. Stabilize Your Everyday Budget

You can’t control national inflation, but you can control how exposed your personal budget is to price shocks.

- Prioritize essentials: Track what portion of your income goes to housing, food, transportation, and healthcare. Small changes (like meal planning, bulk buying staples, or renegotiating recurring bills) can create real breathing room.

- Build an emergency cushion: Even a few weeks’ worth of expenses in savings can prevent inflation-driven surprises (like a higher utility bill) from forcing you into high-interest debt.

- Lock in predictable costs where possible: Fixed-rate loans, longer-term leases, or annual billing discounts can reduce your vulnerability to sudden increases.

2. Invest Like Inflation Will Show Up Again

Inflation tends to arrive in waves. Even if today’s rate slows, it’s wise to assume prices will keep rising over the long run.

- Own productive assets: Broad stock market funds, shares of resilient companies, or diversified portfolios have historically outpaced inflation over long periods.

- Balance growth and safety: A mix of stocks, high-quality bonds, and possibly inflation-linked securities can help manage risk while still targeting growth above inflation.

- Avoid sitting on too much idle cash: Keeping some cash for emergencies is smart; leaving large sums uninvested for years in low-yield accounts is not.

3. Negotiate Your Personal “Inflation Adjustment”

If your expenses are rising, your income strategy may need an update.

- Ask for raises based on value, not just cost of living: Use your achievements at work as leverage while also acknowledging rising living costs.

- Develop additional income streams: Freelancing, part-time consulting, or small side projects can add resilience if your primary salary doesn’t keep pace.

- Invest in skills, not just in markets: Certifications, training, or education that increase your earning potential can be one of the best inflation hedges.

4. Mindset Hacks: Taming Your Own Animal Spirits

One of the most overlooked tools in an inflationary environment is your own mindset. You can’t edit the CPI, but you can adjust how your animal spirits respond to it.

- Focus on trends, not headlines: Don’t let one scary news cycle drive your entire financial strategy.

- Avoid panic buying and panic selling: Whether it’s groceries or stocks, decisions driven by fear are rarely optimal.

- Use rules instead of moods: Automate saving and investing, so your long-term plan doesn’t depend on how you feel about the latest inflation number.

Real-World Experiences: Animal Spirits in an Inflationary World

To really understand how inflation and animal spirits interact, it helps to zoom in on everyday life. Data tells one story; human experiences tell another. Here are a few illustrative scenarios that echo what many households and investors have lived through in recent years.

A Family at the Grocery Store

Picture a family that used to spend $150 a week on groceries. Over a few years, that bill creeps up to $190without anyone buying fancier food. The parents notice they’re putting back snacks, scaling down brand choices, and trimming anything that isn’t strictly necessary.

On paper, their income has risen. But emotionally, it feels like retreat: fewer treats for the kids, less flexibility in the budget, more stress at the checkout line. Their animal spirits respond by becoming cautious. They postpone vacations, delay big purchases, and start treating every nonessential expense as a small luxury that needs justification.

A Small-Business Owner Wrestling with Prices

Now think about a café owner. Her costs have risen: coffee beans, milk, rent, and wages for her staff. She knows she technically has to raise menu prices to stay profitable, but she also fears backlash from customers.

Inflation forces her into tough decisions:

- Raise prices and risk losing regulars who are already feeling squeezed.

- Keep prices low and watch profit margins vanish.

Her animal spirits swing between optimism (“If I improve quality, people will understand higher prices”) and anxiety (“What if people think I’m greedy?”). That emotional roller coaster is part of the broader story behind “everyone hates inflation”: it doesn’t just affect consumers; it stresses out the very businesses trying to serve them.

A Retiree on a Fixed Income

Consider a retiree living on a combination of Social Security and a modest pension. For years, her budget felt comfortable. Then, as prices jump, familiar routines become noticeably more expensive: dining out, medications, utilities, and property taxes all creep higher.

She starts cutting back: fewer restaurant visits, more attention to coupons, a little less help hired for yard work or house cleaning. She’s not in immediate crisis, but she feels less secure. Her animal spirits translate inflation into worry: “What if this keeps going? Will my savings last?”

This anxiety can push retirees to become either overly conservative with their investments (fearing any loss) or overly aggressive (chasing higher returns to “catch up” with inflation). Both extremes carry risk.

A Young Investor Learning in Real Time

Finally, imagine a young professional who started investing just before inflation picked up. They were told to expect steady returns and “normal” markets. Instead, they’ve experienced price spikes, interest rate hikes, and market volatility.

At first, they’re excited: rising wages, a strong job market, and online communities cheering on every dip-buying opportunity. Then inflation bites: rent jumps by hundreds of dollars, groceries cost more, and student loan payments restart. That enthusiasm cools into skepticism.

This investor’s animal spirits cycle through optimism, disappointment, and cautious realism. Over time, if they stick with it, they learn a crucial lesson: inflation isn’t a glitchit’s a recurring feature of the economic landscape. The goal isn’t to predict every twist; it’s to build a plan that bends without breaking.

Across all these experiences, a pattern emerges: inflation doesn’t just alter balance sheets; it shifts moods, confidence, and everyday choices. That’s animal spirits in actionand understanding that dynamic is the first step toward responding with more wisdom and less panic.

Conclusion: Keep Your Cool While Prices Run Hot

“Everyone hates inflation” isn’t just a catchy title; it’s a blunt description of how people feel when their money doesn’t stretch as far as it used to. Inflation stirs up frustration, anxiety, and a sense that the economic game is stacked against ordinary people.

But animal spirits are a two-way street. The same human psychology that fuels panic can also fuel resilience. When you understand how inflation affects both your emotions and your finances, you can respond with more intention:

- By anchoring your budget around essentials and minimizing avoidable vulnerabilities.

- By investing for the long term in assets that have a chance to outrun inflation.

- By strengthening your earning power and diversifying your income sources.

- By creating simple rules that keep your financial plan steady when the headlines are anything but.

Inflation will likely never be popular. But with a bit of common sense, some thoughtful planning, and a clear-eyed view of your own animal spirits, it doesn’t have to be the villain that ruins your story. It can just be one more challenge in an economic world you’re fully capable of navigating.

sapo: Inflation doesn’t just raise pricesit stirs up emotions, warps confidence, and tests every line of your household budget. In this in-depth guide inspired by the spirit of “Animal Spirits: Everyone Hates Inflation” from A Wealth of Common Sense, we unpack why inflation feels so unfair, how animal spirits turn price changes into powerful narratives, and what practical steps you can take to protect your purchasing power. From real-life examples of families, retirees, and small-business owners to common-sense investing and budgeting strategies, this article shows you how to keep your cooland your long-term planintact while prices run hot.