Table of Contents >> Show >> Hide

- What This 6x ARR Headline Actually Means

- The Great SaaS Reset: From Hype Premium to Fundamentals Premium

- Why So Many Public SaaS Companies Are Trading Below 6x

- Who Still Deserves Premium Multiples?

- What the Market Is Really Saying With a Sub-6x Multiple

- Specific Market Signals Worth Watching

- What Founders, CFOs, and Boards Should Do About It

- Why This Is Not the End of SaaS

- The Experience of Operating in a Market Where Half of Public SaaS Trades Under 6x ARR

- Conclusion

Once upon a time, SaaS founders could whisper “recurring revenue” into a pitch deck and watch valuation multiples levitate like party balloons. Those days are gone. Or, more accurately, those days have been dragged into a fluorescent-lit conference room and asked to explain their net revenue retention. Today, the headline that half of public SaaS companies trade at under 6x ARR is not just a spicy market stat. It is a giant neon sign telling operators, investors, and boards that the rules have changed.

The modern SaaS market is no longer paying simply for the promise of growth. It is paying for efficient growth, durable expansion, credible AI strategy, and a business model that does not panic when customers scrutinize budgets. In other words, Wall Street still likes software. It just no longer wants software with a champagne budget and decaf fundamentals.

What This 6x ARR Headline Actually Means

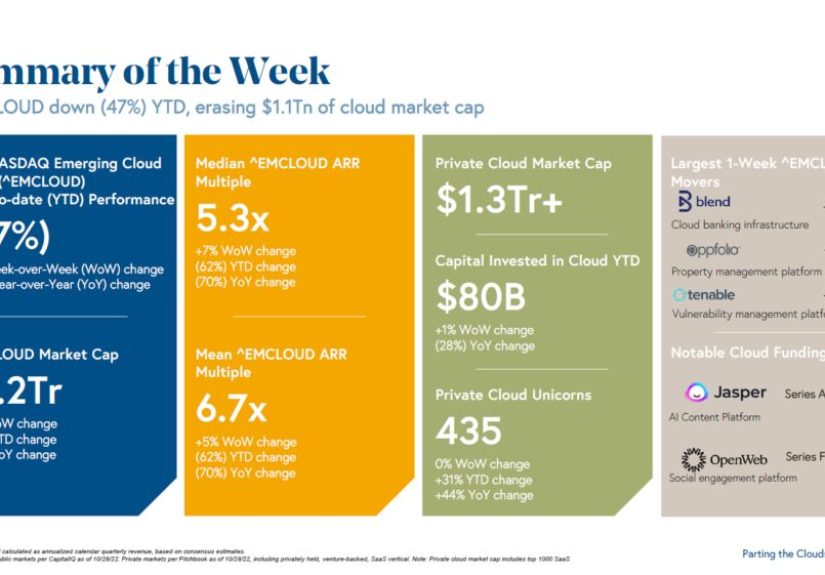

Before we go any further, a quick reality check: in public markets, software companies are often discussed in terms of forward revenue multiples rather than pure ARR. But in SaaS shorthand, founders, investors, and operators often use ARR and revenue multiple language interchangeably when discussing comparable valuations. The big idea is the same. A huge share of public cloud and SaaS companies now trade at levels that would have felt almost insulting during the 2020–2021 boom.

That matters because valuation is not just a scoreboard for public companies. It sets the tone for private rounds, M&A expectations, board conversations, hiring plans, and even how aggressively a company can spend to acquire customers. When public comps compress, the entire software ecosystem suddenly remembers that math exists.

The Great SaaS Reset: From Hype Premium to Fundamentals Premium

The easiest way to understand today’s public SaaS valuation climate is to stop comparing it to the boom years and start comparing it to a more sober normal. The market has not “given up” on SaaS. It has repriced it. Investors are no longer willing to assume that every recurring-revenue business will glide from growth to glorious cash flow without turbulence.

During the zero-interest-rate era, software names benefited from a generous narrative: land customers, grow fast, expand seats, cross-sell modules, and eventually produce handsome margins. That story worked beautifully when capital was cheap, budgets were expanding, and software spend felt nearly automatic. But the market changed. Rates rose. Budgets tightened. Procurement got crankier. Expansion slowed. Suddenly, the difference between a great SaaS company and a merely decent one stopped being theoretical.

That is why the phrase “under 6x ARR” is so important. It signals that the middle of the market has been repriced. Companies that are growing modestly, carrying weaker retention, or struggling to prove AI monetization are no longer being graded on optimism. They are being graded on evidence.

Why So Many Public SaaS Companies Are Trading Below 6x

1. Growth is slower, and slower growth gets punished fast

Public investors will still pay premium multiples, but usually only for companies that combine strong top-line expansion with clear operating discipline. The problem is that many public SaaS companies simply are not growing fast enough anymore to justify premium pricing. In a slower market, “solid” has become a suspicious adjective. Plenty of companies are still growing, but not at a pace that makes investors feel they are buying into a category winner.

2. Net revenue retention is no longer doing all the heavy lifting

SaaS used to enjoy a lovely little trick: even if new customer acquisition slowed, strong expansion from the installed base could keep the machine humming. But net revenue retention has cooled across much of the sector. That means fewer easy expansion dollars, less forgiveness for soft new bookings, and more skepticism around long-term cash flow assumptions. When NRR softens, the fantasy that every subscription model is a forever-compounding annuity starts to wobble.

3. AI is boosting some companies and confusing everyone else

AI has not created one software market. It has created at least three. First, there are companies seen as direct AI beneficiaries. Second, there are incumbents trying to attach AI features to existing products without blowing up margins or pricing logic. Third, there are firms the market worries may be quietly disrupted by AI-native alternatives. Guess which bucket gets the warmest multiple?

Investors increasingly want proof that AI is not just a keynote theme but a monetizable capability. If a company can show customers measurable ROI, product differentiation, and pricing power, the market listens. If the AI strategy sounds like “we added a button and made the demo shinier,” the market reaches for the discount bin.

4. Efficiency is not optional anymore

The Rule of 40 has moved from nice talking point to real valuation filter. Public markets now reward businesses that balance growth and profitability rather than treating profits as a distant hobby. Efficient growth has become the cleanest signal that a company is not just growing, but growing responsibly. That shift is one reason valuation dispersion is so wide today. The market is willing to pay for resilience, not just ambition.

5. The software budget is being reallocated, not simply expanded

One of the most interesting dynamics in today’s market is that IT budgets are not collapsing across the board. They are being redirected. Some dollars that might have once gone to conventional software categories are now flowing into AI tools, infrastructure, and broader transformation initiatives. For many traditional SaaS vendors, that creates a nasty combination: slower seat growth, tougher renewal conversations, and more pressure to justify every line item.

Who Still Deserves Premium Multiples?

The good news is that premium valuations have not disappeared. They have become exclusive. The market still rewards public SaaS companies that check several boxes at once:

- Strong and durable revenue growth

- Healthy free cash flow or a believable path to it

- Net revenue retention that signals real product expansion

- Clear category leadership or defensible niche positioning

- An AI strategy tied to monetization, not decoration

- Credible Rule of 40 performance

That last point matters a lot. Efficient growth is not just finance-team poetry anymore. It is central to how investors separate premium software businesses from the broad pack trading at compressed multiples.

What the Market Is Really Saying With a Sub-6x Multiple

A sub-6x ARR or revenue multiple does not automatically mean a public SaaS business is bad. It often means the market sees one or more of the following:

- The company is maturing faster than its story suggests.

- Retention quality is not strong enough to support long-duration optimism.

- Margins are too weak relative to growth.

- The category faces real AI disruption risk.

- Management has not yet proven it can create durable compounding from here.

Put differently, the market is no longer paying premium prices for “good software company, probably fine.” It wants “excellent software company, clearly differentiated, financially disciplined, and still capable of outgrowing the category.” That is a much harder standard, which is exactly why so many public names now sit under 6x.

Specific Market Signals Worth Watching

Recent market examples make the spread obvious. Stronger names tied to compelling stories and sturdier economics have still achieved healthier multiples, while the broader pack has remained compressed. That is why some recent public software examples have landed around roughly 7x to 11x ARR or revenue, while median market snapshots from software trackers and investors have hovered far lower. There is no single market multiple anymore. There is a wide canyon between the winners and everybody else.

The top tier can still command premium pricing when it combines scale, growth, and margin quality. Meanwhile, average companies are being treated much more like average companies. Shocking, I know.

Another important nuance is that private SaaS and SaaS M&A markets are reading from the same mood board. Buyers still care about growth, but they are increasingly focused on retention quality, profitability, concentration risk, and how believable the future cash-flow story really is. Public market weakness has not destroyed software dealmaking. It has made it far more selective.

What Founders, CFOs, and Boards Should Do About It

Tell a better quality-of-revenue story

Not all ARR is created equal. Investors want to know whether growth comes from sticky customers, real expansion, multi-product adoption, and predictable renewals. If the business has weak retention hidden behind aggressive sales tactics, the market usually figures it out eventually. Usually at the worst possible moment.

Stop treating margin improvement like betrayal

There is still a strange emotional resistance in some corners of software to profitability, as if improving margins means giving up on growth. The market does not see it that way. In today’s climate, better margins often increase strategic flexibility. Efficient companies can keep investing while weaker ones spend half the year explaining why they missed plan by “just a little.”

Be precise about AI monetization

If AI is part of the story, management teams need to explain how it affects pricing, usage, margins, and customer outcomes. Consumption pricing, seat-plus-usage models, and outcome-based packaging are becoming more relevant. Investors do not need every answer today, but they do want evidence that the company understands where the business model is headed.

Optimize for trust, not just narrative

In a compressed valuation environment, credibility is worth a lot. Companies that forecast conservatively, communicate clearly, and show consistent execution tend to earn more patience from the market. Companies that promise moonshots and deliver PowerPoint dust do not.

Why This Is Not the End of SaaS

Let’s be clear: lower multiples do not mean SaaS is broken. They mean SaaS is maturing. Investors now understand that software is not one monolithic category where every recurring-revenue model deserves a heroic multiple. Different segments have different economics. Different categories face different AI risks. Different growth profiles deserve different prices.

In a strange way, this is healthy. A more disciplined market forces better behavior. It rewards products that create measurable value, pricing that matches usage, and operating models that can survive without fantasy financing. That may be less fun than 2021, but it is far better for building real companies.

The Experience of Operating in a Market Where Half of Public SaaS Trades Under 6x ARR

Here is the part spreadsheets cannot fully capture: what this environment feels like inside an actual software company. When half of public SaaS trades below 6x ARR, the mood changes everywhere. Founders feel it when they meet investors who used to ask about TAM first and now ask about burn, expansion, and pricing discipline before the second coffee arrives. CFOs feel it when quarterly planning shifts from “How fast can we hire?” to “Which investments create the fastest and most durable payback?” CROs feel it when customers who once bought extra seats with a shrug now want detailed ROI cases, tighter contracts, and proof that the product will not be replaced by an AI workflow six months from now.

Product teams feel it too. In the old playbook, shipping more features often felt like enough. In the current one, features need to drive adoption, usage, and measurable economic value. Teams are being asked harder questions: Does this improve retention? Does it expand wallet share? Does it justify pricing? Does it make the product more defensible in an AI-shaped market? “Cool demo” is no longer a strategy. It is a nice start, followed immediately by several unpleasant finance questions.

Employees experience the reset in quieter ways. Equity packages are still meaningful, but people are more realistic about what those shares might be worth and how long value creation may take. Boards are less impressed by vanity metrics. Headcount plans are scrutinized more carefully. Marketing teams must prove pipeline quality, not just volume. Customer success teams suddenly become more strategic because expansion and retention are now existential valuation drivers, not post-sale housekeeping.

There is also a psychological shift. A company trading or benchmarking below 6x ARR cannot rely on market sentiment to flatter its story. It has to earn belief quarter by quarter. That creates pressure, but it also creates clarity. Teams begin to focus on the fundamentals that actually compound value: better retention, stronger product-market fit, cleaner pricing, smarter segmentation, and capital allocation that does not assume infinite forgiveness.

And yet, there is a silver lining. Operators who build through this kind of environment often emerge stronger. They learn how to run a tighter company. They learn that durable growth beats theatrical growth. They learn that customers renew when value is obvious, not when branding is loud. They learn that AI should improve the business model, not just the homepage.

So yes, half of public SaaS trading under 6x ARR sounds gloomy. But it is also a forcing function. It separates software businesses that merely participated in the SaaS era from the ones actually prepared to lead its next chapter. The market may be less generous now, but it is being more honest. In the long run, honest markets tend to build better companies.

Conclusion

“Half of public SaaS companies trade at under 6x ARR today” is not just a catchy market headline. It is a summary of the sector’s new reality. Public investors are still willing to pay up, but only for software businesses that demonstrate efficient growth, durable retention, credible AI monetization, and real financial discipline. The rest are being valued with much less romance and much more scrutiny.

That may sting if you are benchmarking against old multiples, but it is also useful. It tells founders exactly where to focus. Build a stickier product. Improve expansion. Tighten margins. Explain AI with economic clarity. Earn Rule of 40 credibility. In this market, premium valuation is no longer a genre. It is a performance.