Table of Contents >> Show >> Hide

- What “Obamacare cost” really means (and why people get surprised)

- The big factors that change your Obamacare price

- How to estimate your monthly Obamacare premium in about 10 minutes

- Step 1: Define your household (for ACA purposes)

- Step 2: Estimate your household income for the coverage year

- Step 3: Check whether Medicaid might be your better (cheaper) option

- Step 4: Find the “benchmark” premium in your area

- Step 5: Apply the “you’re expected to pay up to X% of income” rule

- Expected premium contribution percentages (Coverage Year 2026)

- Quick reality check: what’s the Federal Poverty Level (FPL)?

- Examples: estimating “How much will Obamacare cost me?”

- The second price tag: deductibles and out-of-pocket maximums

- Don’t let tax time body-slam your budget

- What if I have an employer plan offer?

- When can I enroll, and when does coverage start?

- Ways to lower your Obamacare cost (without becoming a hermit who only eats beans)

- FAQ: fast answers to common “Obamacare cost” questions

- Real-world experiences: what people learn the hard way (and then laugh about later)

- Conclusion

“Obamacare” (the Affordable Care Act) doesn’t have one price tag. It’s more like ordering coffee: your total depends on size, add-ons, and whether you’ve got a coupon you didn’t realize you had.

In practical terms, your ACA cost usually comes down to three buckets:

- Monthly premium (what you pay to keep the plan active)

- Out-of-pocket costs (deductible, copays, coinsurancewhat you pay when you actually use care)

- Tax-time true-up (if you used subsidies, the IRS may adjust based on your final income)

This guide shows you how to estimate your personal cost with real rules, realistic examples, and a few “wish someone told me this earlier” momentswithout turning your brain into applesauce.

What “Obamacare cost” really means (and why people get surprised)

When someone asks, “How much will Obamacare cost me?” they usually mean: “What will I pay each month?” That matters, but it’s only part of the story.

Two people can pick plans with the same monthly premium and still have wildly different total costs by the end of the year because:

- One person barely uses care and mostly wants “just in case” coverage.

- Another person takes multiple prescriptions, sees specialists, or expects a surgery.

So the smarter question is: What will my monthly premium be, and what is my realistic worst-case and typical-case spending?

The big factors that change your Obamacare price

1) Where you live

Marketplace premiums are regional. Even within the same state, prices can vary by county because competition, local health care costs, and plan availability vary.

2) Your age

Under ACA rules, premiums can be higher for older adultsup to a limit (often described as up to 3x compared with younger adults). That’s why a 27-year-old and a 60-year-old can see very different price quotes for the same plan.

3) Tobacco use

In many states, insurers can charge tobacco users more (sometimes a lot more). If you use tobacco, that surcharge can raise the premium you see before any subsidy is applied. (And yes, this can make budgeting… spicy.)

4) Household size and income

Your subsidy eligibilityif you qualifydepends on your household size and your estimated household income for the coverage year (not last year’s income). If your income changes mid-year, your best move is to update your Marketplace application so you don’t get whacked at tax time.

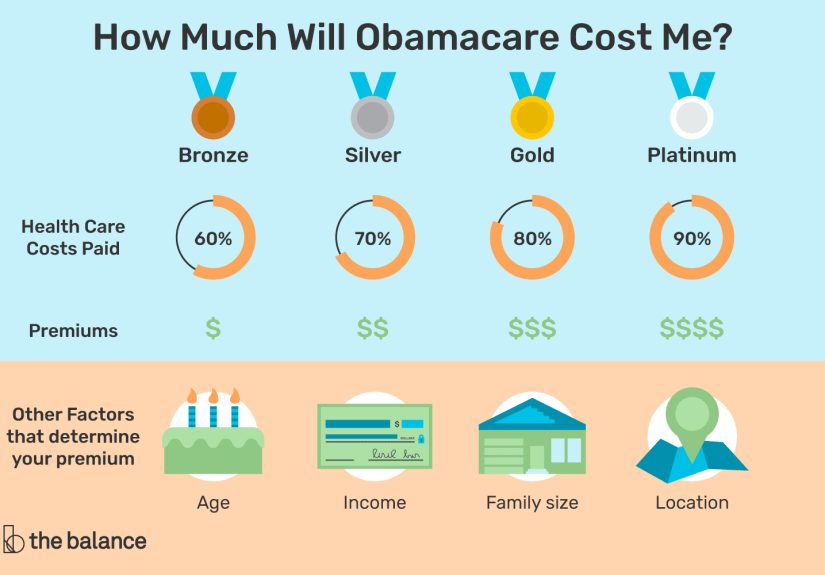

5) Plan level (Bronze/Silver/Gold/Platinum) and network

Metal levels describe how costs tend to be split between you and the plannot how fancy your doctor’s waiting room is.

- Bronze: usually lower premiums, higher deductibles and higher out-of-pocket when you use care

- Silver: the “subsidy math” level (important if you qualify for cost-sharing reductions)

- Gold/Platinum: usually higher premiums, lower costs when you use care

Network type (HMO, PPO, EPO, etc.) and whether your doctors are in-network can also change your real-world spending.

6) Whether you qualify for financial help

Two main types of help can reduce what you pay:

- Premium Tax Credit (lowers your monthly premium if you buy through the Marketplace)

- Cost-sharing reductions (CSRs) (lower deductibles/copays/out-of-pocket max, but only if you choose a Silver plan and meet income rules)

Also, if your income is low enough, you might qualify for Medicaid depending on your state’s rulesincluding whether it expanded Medicaid.

How to estimate your monthly Obamacare premium in about 10 minutes

Step 1: Define your household (for ACA purposes)

Generally, your Marketplace household includes you, your spouse (if you file jointly), and the people you’ll claim as tax dependents. Household rules matter because subsidies are based on household income and size.

Step 2: Estimate your household income for the coverage year

The Marketplace asks you to estimate expected income for the year you want coverage. If you’re self-employed or have variable income, use your best honest estimate and update it if things change. Common income types include wages, self-employment net income, unemployment, Social Security, and other taxable incomedetails vary, so use the Marketplace definitions as your guide.

Step 3: Check whether Medicaid might be your better (cheaper) option

If your income is low enough, you may qualify for Medicaidespecially in states that expanded it. In many expansion states, adults can qualify based on income alone up to roughly 138% of the federal poverty level (FPL).

Step 4: Find the “benchmark” premium in your area

Subsidies are tied to the second-lowest-cost Silver plan available to you (often called the “benchmark”). Your actual plan can be Bronze, Silver, Gold, etc.but the subsidy math starts with that benchmark price.

Step 5: Apply the “you’re expected to pay up to X% of income” rule

If you qualify for the Premium Tax Credit, the Marketplace limits how much you’re expected to pay for the benchmark premium to a percentage of your household income. The government covers the difference as a tax credit (either up front each month or later on your tax return).

Important timing note: Rules can change by year. For coverage year 2026, many tools and official tables reflect a return to higher “expected contribution” percentages compared with 2021–2025 enhanced subsidy levels (unless laws change again).

Expected premium contribution percentages (Coverage Year 2026)

These percentages are used to estimate your maximum benchmark premium contribution if you’re eligible for a Premium Tax Credit:

| Household income (as % of FPL) | Expected premium contribution range (% of income) |

|---|---|

| Less than 133% | 2.10% |

| 133% to <150% | 3.14% to 4.19% |

| 150% to <200% | 4.19% to 6.60% |

| 200% to <250% | 6.60% to 8.44% |

| 250% to <300% | 8.44% to 9.96% |

| 300% to 400% | 9.96% |

Translation to human: the higher your income (relative to FPL), the larger the share of the benchmark premium you’re expected to payup to a cap.

Quick reality check: what’s the Federal Poverty Level (FPL)?

FPL is a federal income guideline used to determine eligibility for certain programs and ACA savings. It changes annually.

For example, the 2025 HHS poverty guideline for a household of 1 in the 48 contiguous states and D.C. is $15,650, and for a household of 2 it’s $21,150. (Different figures apply in Alaska and Hawaii.)

Marketplace eligibility and subsidy math for a given coverage year typically use the most recent available poverty guideline set when rules were published for that cycle, so calculators often show FPL-based income bands for the specific coverage year.

Examples: estimating “How much will Obamacare cost me?”

These are simplified examples to show how the math works. Your exact premium depends on your ZIP code, age, household, tobacco status, and plan availability.

Example 1: Single adult at about 200% FPL

Scenario: You’re single, not using tobacco, and your projected income is about $31,300 (roughly 200% FPL using 2025 guideline figures commonly applied in 2026 coverage-year references).

Expected benchmark contribution (roughly): up to 6.6% of income.

6.6% of $31,300 = $2,065.80 per year, or about $172/month.

Now imagine the benchmark Silver plan in your area for your age costs $600/month. Your estimated Premium Tax Credit could be roughly:

- $600 benchmark premium

- minus $172 expected contribution

- = about $428/month in tax credit

You could then apply that credit to the plan you choose. Pick a cheaper plan? You might pay even less than $172. Pick a pricier plan? You pay the difference.

Example 2: A 50-year-old in a high-cost area

Age and location matter a lot. One congressional analysis shows benchmark premiums for a 50-year-old can range widely by county (hundreds of dollars apart per month). If your benchmark is high, your tax credit (if eligible) can also be largerbecause it’s based on the benchmark.

Key takeaway: Your subsidy is not a flat dollar amount for everyone; it’s tied to the benchmark premium where you live and your income-based expected contribution.

Example 3: Household income over 400% FPL (watch this closely)

Depending on the year’s rules, people above 400% FPL may or may not qualify for subsidies. Many 2026 references assume that households above 400% FPL are ineligible for Premium Tax Credits unless laws are changed.

What that means: If your income is above that cutoff, your monthly cost could jump because you’re paying the full premium. For higher earners in expensive regions (or older adults), “full price” can be a serious number.

The second price tag: deductibles and out-of-pocket maximums

Your monthly premium is the membership fee. The deductible/copays/coinsurance are the cover charge once you actually walk into the club.

Marketplace plans have a federal cap on out-of-pocket maximums for covered in-network essential health benefits. For the 2026 plan year, the Marketplace out-of-pocket limit can be up to $10,600 for an individual and $21,200 for a family (though many plans have lower limits).

Cost-sharing reductions (CSRs): the underrated discount

If you qualify and you choose a Silver plan, CSRs can reduce deductibles, copays, and your out-of-pocket maximumsometimes dramatically.

Think of it like this: a standard Silver plan is decent. A CSR Silver plan can become “Silver-plus,” with cost-sharing that looks more like Gold or even Platinum at lower incomes.

Example: Some CSR eligibility bands can lower the maximum out-of-pocket exposure a lot compared with the standard cap, which can be huge if you actually need care that year.

Rule of thumb: If your income is under the CSR threshold and you expect to use healthcare, don’t automatically chase the cheapest monthly premium. Run the numbers on a CSR Silver plan first.

Don’t let tax time body-slam your budget

If you take the Premium Tax Credit in advance (to lower monthly premiums), you must reconcile it when you file taxes.

Here’s what happens:

- You estimate income when you enroll.

- The Marketplace can apply some/all of your expected credit monthly.

- After the year ends, you get a Marketplace tax form showing what was paid on your behalf.

- You file your tax return and reconcile the credit using Form 8962.

If your actual income ends up higher than estimated, you may have to repay some credit. If it ends up lower, you may get additional credit back. This is why updating income changes during the year is not just “nice”it’s budget protection.

What if I have an employer plan offer?

If you have an offer of employer-sponsored coverage, ACA subsidy eligibility can get complicated fast.

In general: if the employer offer is considered affordable (based on a percentage of household income) and meets minimum standards, you usually can’t get Premium Tax Credits for Marketplace plans.

For 2026 references, the affordability-related percentage used in IRS guidance is 9.96%. The exact application can depend on the type of offer and household situation, so when in doubt, check the Marketplace and tax rules for your scenario.

When can I enroll, and when does coverage start?

Most people enroll during Open Enrollment. For the 2026 Marketplace cycle, the general window has been described as starting November 1 and running through January 15, 2026, with earlier enrollment typically needed for coverage starting January 1 and later enrollment starting February 1 (exact details can vary by state and timing).

You may also qualify for a Special Enrollment Period if you have certain life changes (like losing other coverage, moving, getting married, having a baby, etc.).

Ways to lower your Obamacare cost (without becoming a hermit who only eats beans)

1) Compare total yearly cost, not just the monthly premium

Low premium + high deductible can be a great deal if you rarely use care. It can also be a financial trap if you actually need care. Always scan:

- Deductible

- Out-of-pocket maximum

- Copays/coinsurance for the services you actually use (primary care, mental health, specialist visits, prescriptions)

- Network (are your doctors in it?)

2) If you qualify for CSRs, treat Silver like it’s the VIP line

CSRs only work with Silver plans. If your income is within the CSR range, a Silver plan can deliver far better protection at a similar (or sometimes lower) premium after subsidies.

3) Update your application when income changes

New job, fewer freelance clients, big bonus, divorce, new babythese can all change your subsidy. Updating your Marketplace account helps keep your monthly premium accurate and reduces tax-time surprises.

4) Look at HSA eligibility (especially for 2026)

HSAs can help you pay qualified medical expenses with tax advantages, but you generally need an HSA-eligible high-deductible health plan. Check whether a plan is HSA-compatible before you fall in love with it. Some 2026 Marketplace notes highlight expanded availability of HSA pairing for certain plan types, which can be useful for people who want to save for medical costs.

5) Don’t ignore free preventive care

Many preventive services are covered without cost-sharing when you use in-network providersstuff like screenings and vaccines. Using preventive care can reduce bigger costs later (and it’s one of the few areas in American life where “free” sometimes actually means free).

FAQ: fast answers to common “Obamacare cost” questions

Is Obamacare free?

Sometimes the monthly premium can be very lowor even $0for certain households after subsidies, especially at lower incomes. But most plans still have some out-of-pocket costs when you use care.

Can I buy an ACA plan off the Marketplace?

You can often buy ACA-compliant plans outside the Marketplace, but premium tax credits and CSRs generally require Marketplace enrollment. If you want financial help, shop through the Marketplace route.

What’s the “real” cost if I get sick?

Your maximum exposure is usually capped by the out-of-pocket maximum for covered in-network care. But the path to that cap (deductible, copays, coinsurance) varies. If you expect significant care, the plan’s cost-sharing design matters as much as the premium.

Do I need to pay the first premium?

Yescoverage generally doesn’t start until you pay your first premium. If you enroll and don’t pay, the plan can be canceled for nonpayment.

Real-world experiences: what people learn the hard way (and then laugh about later)

Experience #1: The freelancer who underestimated income.

Jamie is a freelance designer. Some months are feast, some months are “I can’t believe I’m paying for cloud storage again.” Jamie estimated a lower annual income to qualify for a bigger premium tax credit, planning to update it later. Then a surprise contract came in, income jumped, and Jamie forgot to update the Marketplace account. The monthly premium felt great all year… until tax season. Reconciling the advance credit stung because the final income didn’t match the estimate. Jamie’s takeaway: “Update your income the moment you realize the year is going better than expected. Future-you will send you a thank-you card.”

Experience #2: The couple that shopped only by premium.

Morgan and Alex picked the lowest premium plan they could find. Monthly cost: chef’s kiss. Deductible: Mount Everest. When Alex needed imaging and physical therapy after an injury, the “cheap plan” became an expensive lesson. They didn’t hit the out-of-pocket maximum, but they spent far more than they expected because the deductible and coinsurance were steep. Next year, they compared total estimated yearly cost based on likely care and found a plan with a higher premium but lower cost-sharing that was cheaper overall for their situation. Their takeaway: “If you’ll actually use the insurance, the premium is only the trailernot the whole movie.”

Experience #3: The CSR Silver plan that felt like a cheat code.

Priya had income low enough to qualify for cost-sharing reductions. At first, she assumed Bronze was automatically the best deal because the premium looked lower. Then she compared a CSR Silver plan: lower deductible, lower copays, and a much lower “worst case” if she had a bad health year. The premium difference after subsidies was small, but the protection was dramatically better. Her takeaway: “CSR Silver is like discovering your boarding pass comes with free checked bags. Same trip. Way less pain.”

Experience #4: The early retiree watching the subsidy cliff.

Sam retired early and used Marketplace coverage as a bridge to Medicare. Sam learned that the sweet spot for affordability often depends on how income compares to FPLand that a small income bump can change subsidy eligibility in certain rule years. Sam started planning withdrawals more intentionally, building a buffer for years when subsidies might be less generous. Takeaway: “Your ACA cost is not just a health decisionit’s a cash-flow decision.”

Experience #5: The “my doctor isn’t in-network” surprise.

Taylor picked a plan with great benefits and a decent premium, then discovered their favorite specialist wasn’t in the network. Switching doctors was annoying, and paying out of network was worse. Taylor now checks networks first, then shops plans. Takeaway: “A plan you can’t use is just a very expensive PDF.”

Conclusion

So, how much will Obamacare cost you? The honest answer is: it depends on your age, ZIP code, income, household size, tobacco status, and how you use health care.

The useful answer is: you can estimate it quickly by (1) projecting your household income, (2) checking whether you qualify for Medicaid or Marketplace savings, (3) comparing plans by total costs, and (4) choosing a plan level that matches your real lifenot your fantasy life where nobody gets sick and everyone drinks eight glasses of water a day.

When you do it that way, the cost stops being a scary mystery and becomes something you can actually budget forlike an adult. A slightly more informed adult. With better insurance.